ISLAMABAD ( MEDIA REPORT )

Despite a lackluster performance during the second half amid amplified volatility, the stock market delivered a healthy return of 23.2% in FY17 on the back of stellar performance during the period from Jun-Dec 2016. During FY17, our flagship NAFA Stock Fund (NSF) has delivered a 33.7% return to our investors, thus out-performing the stock market by 10.5%. This return is net of management fee and all other expenses.

We attribute subdued performance of the stock market during the second half of FY2017 to heightened political uncertainty, large foreign net selling to the tune of USD332 million, and mounting risks to the Balance of Payment position. Elevated domestic political uncertainty linked to Panama Leaks case remained on the forefront, sending jitters in the market.

Adding to the local market participants woes was a cumulative net foreign out-flows of USD133 million during May and June 2017, contrary to the market expectation of sizeable inflows from the tracker funds amid reclassification of PSX into widely followed MSCI Emerging Market Index. The stock market has declined by 11.9% from its peak hit on May 24, 2017.

In near term, we reckon that political noise is expected to remain elevated due to expected Panama leaks judgment, and repercussions of this unprecedented case on the upcoming elections. However, as schedule for the upcoming elections draws near, this uncertainty is likely to gradually subside, in our view. Setting aside election related priorities, the incoming government in its first year is expected to embark on the stalled economic reforms, and will also have a mandate to negotiate with multilateral agencies to secure a financing package.

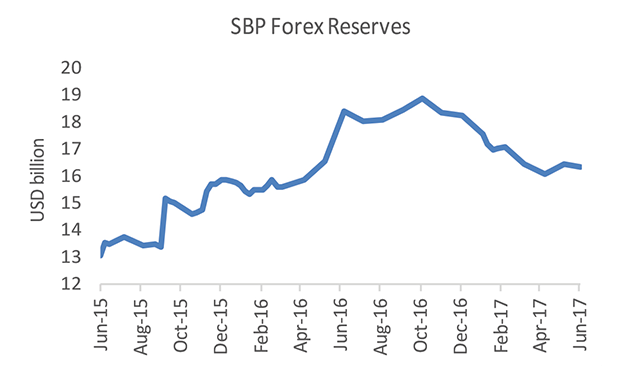

A genuine concern about the economy is how the government will manage surging trade and current account deficits. In our view, in addition to lowering the cost of doing business, a key remedy in this regard is measured PKR devaluation, which would help in arresting non-essential imports, and augment exports to some extent by partially restoring our international competitiveness. The government has so far resisted this step due to political consideration as this is expected to have a negative impact on inflation, interest rates and debt servicing costs. However, given hefty rise of 39% YoY basis in the trade deficit during 11MFY17, and consequent pressures on forex reserves, some devaluation is inevitable.

It is very difficult, if not impossible, to time the stock market. Therefore, we suggest our investors hold their positions in the stock market/funds, and wait for the stock market to gradually recover in FY18.